An Introduction to Private Placement Life Insurance (PPLI)

Private Placement Life Insurance (PPLI) is a "Super Roth" for wealthy individuals that allows them to accumulate wealth free from income and estate taxes.

So in our last post we covered the difference between income taxes and estate taxes and how moving assets outside the estate to save on estate taxes exposes clients to income taxes that they otherwise wouldn’t have to pay due to loss of step-up in basis.

So what’s worse?

Paying estate taxes on your net worth above $30M?

Or your beneficiaries having to pay income taxes on all your gains due to loss of step-up in basis?

This is a math and planning question that depends on both your projected net worth and projected tax-rates now and in the future.

But what if you could save on both estate taxes AND income taxes through proper planning?

That’s what this post is about.

To maximize the value of financial planning you have to “stack” financial planning opportunities.

")

It’s one of those “the sum is greater than the individual parts” type thinking.

Steve Wozniak was a phenomenal technical computer programmer but had no business acumen.

Steve Jobs on the other hand had great business vision, marketing and storytelling abilities but limited technical abilities.

Individually you would have probably never heard of any of them.

But collectively they created Apple.

The same can be thought of here.

Estate planning vehicles can minimize your estate tax liabilities but expose you to income tax liabilities that might not be worth it.

Life insurance vehicles on the other hand can help save you on income taxes, but will be subject to the estate tax if not owned by an estate planning vehicle.

But the combination of the two allows you to save on both estate taxes and income taxes.

But in order to understand the value of this it’s important to understand some of the vehicles in play.

We spoke about estate planning vehicles in the last post and the value that they can have.

In this post we’re going to talk about a life insurance vehicle called Private Placement Life Insurance (PPLI).

What is Private Placement Life Insurance (PPLI)?

Private Placement Life Insurance (PPLI) is a life insurance vehicle that allows the growth in the underlying investments in the vehicle to be tax-free.

This tax-free growth feature is not unique to PPLI.

All life insurance vehicles allow for this.

The three key differences between PPLI and traditional life insurance are:

1) Access to private funds that are not available to the average investor

2) Ability to select your own investment advisor to choose the underlying investments

3) Significantly lower costs

1) Access to private funds that are not available to the average investor

PPLI allows clients the ability to invest in high growth funds that the average investor doesn’t have access to within a traditional life insurance vehicle.

Most funds available to invest in within a traditional life insurance vehicle are for the average middle class investor to understand so that they can allocate a few thousand dollars to it.

However, the funds available to invest in within a PPLI policy are made with the qualified purchaser ($5M in net worth and above) to invest in. These are typically funds from large fund managers like Millenium, Golub Capital, Ares, Goldman Sachs, JP Morgan, Blackstone, Bain Capital and more.

Also, since these funds are geared towards the ultra-wealthy they often have investment minimums of $250k-$1 million just to be able to invest in the fund.

Contrast this to a simple Vanguard ETF in which you can buy fractional shares for a $1.

So these class of funds are for a different class of investor entirely.

The other huge benefit of investing in private funds through PPLI is that most of these private funds would otherwise be heavily taxed at ordinary income rates. So for investors who already like/invest in these funds it makes more sense to invest in through a tax-free wrapper.

Contrast this to most funds on the traditional life insurance platform which are just derivatives of a tax-efficient S&P500 fund with significantly higher expense ratios—which is another key reason why I’m not a fan of most traditional VUL policies.

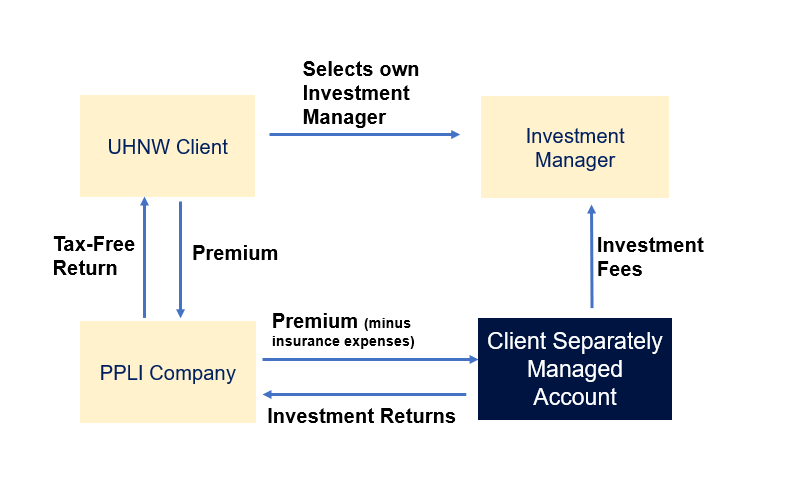

2) Ability to select your own investment advisor to choose the underlying investments

Some UHNW clients might not like the investment offerings I mentioned above or the rest of the offerings on the existing platform. What PPLI allows is for the client to choose their own investment adviser. The investment advisor then just has to get approved by the insurance company as an outsourced investment advisor.

You can think of it as the insurance company outsourcing the investment responsibility of the contract to an investment advisor of your choosing.

So instead of you being forced to use that insurance company for both the insurance piece and the investment piece, they keep the insurance piece and outsource the investment piece to an investment advisor that you pick.

1) Lower insurance costs

Perhaps the biggest benefit of PPLI is the lower insurance costs of PPLI versus traditional life insurance. The insurance costs for PPLI are generally 0.5%-1% of the market value of the assets versus 1.2%-1.5% of the market value of the assets for a traditional life insurance policy.

The reason for this has to do with economies of scale.

Traditional life insurance is sold to the mass life insurance market which are paying average annual premiums of ~$10k-$20k/year.

And the first year commission paid to the agent who sold it is roughly 80%-100% of that first year premium.

What this means is that the insurance company is at a heavy loss in the early years of a traditional policy.

And they recoup this with higher expenses throughout the life of the policy.

PPLI is a fundamentally different business model.

It’s ripping out the large upfront commissions and expenses for an assets under management play on a larger amount of assets.

Instead of taking in smaller amounts in premiums, PPLI companies and brokers are taking in larger amounts of premiums (often $5M+) in exchange for a smaller ongoing fee on the back-end.

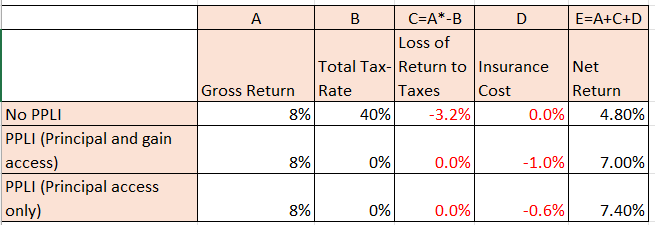

For those trying to understand what the costs of PPLI are, they depend on whether you want the principal back or principal and the gains back.

For example, let’s say you want to invest $10M into a PPLI structure and you expect it grow to $30M.

If you only want to access $10M and leave the remaining $20M of growth to the next generation, then the costs are going to be closer to 0.60% of the assets in the vehicle.

On the other hand, if you want to access all of the $10M principal and ~90% of the $20M growth then the costs are going to be closer to 1% of the assets in the vehicle.

PPLI costs vs Taxable Account Taxes

Who is Private Placement Life Insurance For?

Before we get too far into how to think about positioning private placement life insurance as part of a holistic wealth management plan, I think it’s important to understand who is a good candidate for using this tool:

1) Is a Qualified Purchaser (i.e. has a net worth of $5M+ excluding personal residence) and ideally has $15M+ net worth

2) Is willing to invest $2M+ into the vehicle

3) Doesn’t need access to the funds for at least 10 years

4) Understands that only high-earning, tax-inefficient assets are a good fit for this vehicle

5) Is willing to give up investment control of the assets to another party

6) Understands that in order to maximize the value of PPLI it should be part of a holistic estate plan

7) Understands the value of offshore vs onshore PPLI

The first 3 points are pretty straightforward. The vehicle is really only available for ultra wealthy clients who are willing to invest a large amount into the vehicle. And given that it’s a tax-free vehicle, the highest value comes from allowing assets to compound in the vehicle tax-free for the longest time possible.

If you’re only trying to use the vehicle for a short period of time then it doesn’t really make as much sense (unless of course you are expecting a very large taxable gain during that time you are hoping to avoid).

Clients can access 85%-90% of both the principal and gains in PPLI (and unlike a Roth IRA they don’t have to wait until age 59.5).

However, if you only invest in the vehicle for a few years there won’t be much gains in the policy by the time you start to take the funds out.

Understands that only high-earning, tax-inefficient assets are a good fit for the vehicle

I see a lot of clients wanting to invest in basically an S&P500 fund within a PPLI vehicle. And while you can do that, it’s largely a waste of the vehicle. As we talked about in previous posts you can buy and hold an S&P500 fund and pay very little in taxes and have all of the gains pass to the next generation tax-free through step-up in basis. You don’t need a PPLI vehicle to do this.

If you’re going to make maximum use of the vehicle, you want to invest in assets that are both tax-efficient and high-earning. That way you are getting the maximum amount of after-tax growth from using the vehicle.

So it’s important that clients think about asset location prior to purchasing a PPLI policy.

If the underlying investment is tax-efficient to begin with, then investing in the underlying investment fund within a tax-free vehicle doesn’t make sense.

For example, if your goal is to buy and hold an S&P500 fund within a PPLI vehicle this doesn’t really make sense.

Remember that most of the S&P500 gains each year are unrealized gains. This means you’re not paying taxes on these gains. You only pay taxes on them when you sell.

This is my main problem with traditional VUL life insurance policies.

Most of the options available are derivatives of an S&P500 fund—except with higher expense ratios and turnover ratios.

If I’m primarily going to invest in the S&P500 for the long-run and have my kids inherit it tax-free through step-up in basis, then it’s a buy and hold investment with both a low expense ratio and low taxability.

Why would I want to put this in a tax-free vehicle with higher investment and insurance expense ratios when me and my children would basically be getting this tax-free to begin with?

Any type of VUL (including PPLI) only makes sense if I’m investing in tax-inefficient funds (i.e. funds that have a high tax-rate and are taxed on an annual basis instead of a tax-deferred basis).

Putting a Tax-Efficient Asset within PPLI

1) Is willing to give up investment control and invest in a diversified strategy

PPLI is often thought of as a “Super Roth” for wealthy individuals because of the tax-free nature of the growth.

However, it’s not a “Self-Directed Super Roth IRA”.

In other words, someone else besides the client has to manage the investment assets here.

The client is allowed to select the overall investment strategy, but someone else must actually execute the strategy, choose the actual assets being purchased and then make the trades.

And the investment strategy must be a diversified one—i.e. it can’t be “invest 100% in Bitcoin and YOLO it”.

So for example, let’s say I’m the client and I want to invest in private credit funds.

I can work with my investment advisor to craft an investment policy statement that focuses on private credit investments.

The private credit investment strategy must be invested in multiple private credit strategies without it being overconcentrated in any one position (the actual requirements are that no more than 55% of the funds be invested in one position, no more than 70% be invested in two positions, no more than 80% invested in three positions, and no more than 90% invested in four positions).

However, the investment advisor must be the one that is actually choosing the individual private credit positions to invest in—not me.

Understands that in order to maximize the value of PPLI it should be part of a holistic estate plan

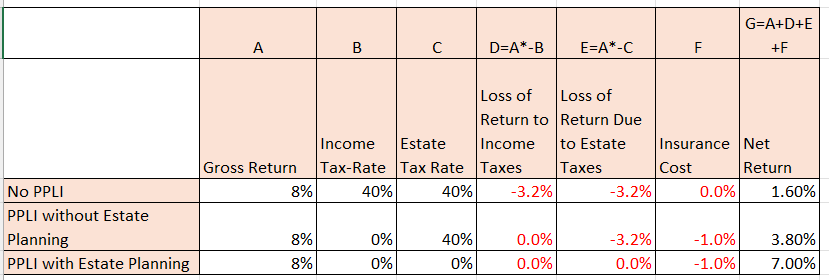

In addition to the points above, it’s important to understand the importance of including PPLI as part of an estate plan.

Sure PPLI on its own solves the maximization of after-tax returns when we think about income taxes.

But if this PPLI policy isn’t owned by an estate planning vehicle, then all of the principal and gains will be subject to a 40% estate tax.

Setting up a PPLI policy that saves on income tax only to lose all of that savings (and potentially more) to the estate tax seems like a waste of effort.

So think about PPLI as a tool as part of a larger estate and wealth management plan where tax-efficient assets like an S&P500 fund are within your estate and tax-inefficient assets like private credit, hedge funds, alternative investments and high growth private equity assets are outside your estate and in an income tax-free wrapper.

That way you’re getting estate and income tax protection.

The Value of Stacking Income and Estate Planning Opportunities

1) Understands the value of offshore vs onshore PPLI

Anytime offshore PPLI gets mentioned, people associate it with people moving money overseas to launder money. But the difference between offshore and onshore PPLI has a lot more to do with regulation vs flexibility in the same way that here in the U.S. there are general federal government precepts that need to be followed while allowing individual states flexibility with how certain laws are applied.

The same can be said with onshore vs offshore PPLI. Onshore PPLI comes with a lot more regulation and strict adherence to federal government terms, whereas offshore PPLI must abide by larger overarching principles for life insurance but give leeway to how some of the minutia of those laws are applied.

In fact, many offshore carriers file what’s known as a 953d election that means that they are treated as a U.S. taxpayer.

In other words, 953d carriers have to follow some overarching U.S. rules that govern what a life insurance policy is. They are just allowed flexibility on how some of the underlying very specific life insurance rules are applied.

Onshore carriers on the other hand aren’t afforded that same flexibility.

And as is always the case with more regulation, onshore PPLI has more consumer protections with regards to who can qualify for the product and what can be invested in within the policy whereas offshore PPLI allows for more flexibility with what can be invested in within the policy.

So where onshore PPLI affords more regulation at the expense of more costs and strict limitations, offshore PPLI afford more flexibility at the expense of better customer service and more strict due diligence.

So for those looking for cookie cutter, one size fits all solutions with notably more red tape and expenses but an overall better user experience—onshore PPLI is often a better fit.

But for the more sophisticated investor who is willing to exchange a better user experience for better pricing and more flexibility in crafting solutions that are more customized to that person’s goals, offshore PPLI affords a wider range of exciting possibilities—some of which we’ll be exploring in our next post.

About the Author

Rajiv Rebello is the Principal and Chief Actuary of Colva Insurance Services and Guaranteed Annuity Experts. He helps HNW clients implement better after-tax, risk-adjusted wealth and estate solutions through the use of strategic planning and life insurance and annuity vehicles. He can be reached at rajiv.rebello@colvaservices.com.

You can also book a call directly with him here: