Separating Value from Bias in the Realm of Finance and Insurance

Separating Value from Bias in the Realm of Finance and Insurance

When we have limited ways to actually measure the value of our purchases, our biases make us feel like it’s there

I’ve been working in the personal finance/investment/insurance/retirement planning field for the last 17 years now and I’ve found that the average client who utilizes financial advisors, insurance products, or complicated alternative investments really doesn’t understand how to properly assess the value of the service or product they purchased.

They have an idea in their head of what they think they should be getting, but don’t really have a way to measure the value that it is adding (or subtracting) from their lives.

And this makes sense if you think of the product or services here that are being offered versus the typical consumer products we purchase.

If I sell you a typical consumer product like a car, over time you can determine if it works properly or whether it breaks down more than you expected it to.

You don’t have to be an expert on cars to be able to do this.

On top of that, most people can also distinguish the difference in the quality of the ride between a Tesla Model S and a Toyota Prius.

But if I’m a financial advisor selling you my services or an insurance product, what frame of reference do you have of ascertaining whether the service or product is operating the way it’s supposed to or is better or worse than other products/services available?

How can we tell if we’re getting a Toyota Prius financial advisor/insurance product but paying a Tesla Model S price for it?

How can we tell if we purchased the equivalent of a lemon car if we’re not qualified enough to look under the hood?

Using Emotional Biases to Distort Logic and Justify Financial Decisions

The truth of the matter is that unless we’re well versed in personal finance, tax law, estate planning, insurance, investment management, and more importantly, how all of these need to be integrated together as part of a cohesive plan, then we can’t.

And since even basic financial literary is not taught in our primary education system, even those of us who are successful in other fields aren’t really qualified to assess both the value and risk of a field that is entirely different than our own.

Being an expert in our own field doesn’t necessarily translate to our ability to assess the validity of an expert in another.

Holistic Financial Planning Involves Integrating Individual Expertise

For the most part, we base our purchase decision of financial services on a combination of how the person selling the product/financial service makes us feel and how much that salesperson appeals to our preexisting biases that we bring to the table.

The actual “finance” part of the equation is largely irrelevant. If we feel strongly about how the story told to us by the salesperson made us feel, we’ll rely on confirmation bias to make us feel that the numbers presented to us are somehow sound.

It doesn’t actually matter to us what the numbers or value proposition actually say about risk and return.

What really matters is how we are made to feel both about the salesman and the idea he is selling.

And this is why financial services/insurance products are services that are “sold” by the salesman more than “bought” by the consumer.

We’re not paying for the best financial decision for our situation; we’re paying to feel the most comforted about the financial decision we make.

Maya Angelou actually has a great quote about human interaction that encapsulates this:

“I’ve learned that people will forget what you said, people will forget what you did, but they will never forget how you made them feel.”

-Maya Angelou

While this sentiment is absolutely beautiful on a personal level, it can be deeply problematic on a business level.

And that’s because the people who make us feel the best about the decision we make aren’t always the same people who help us make the best decision for us.

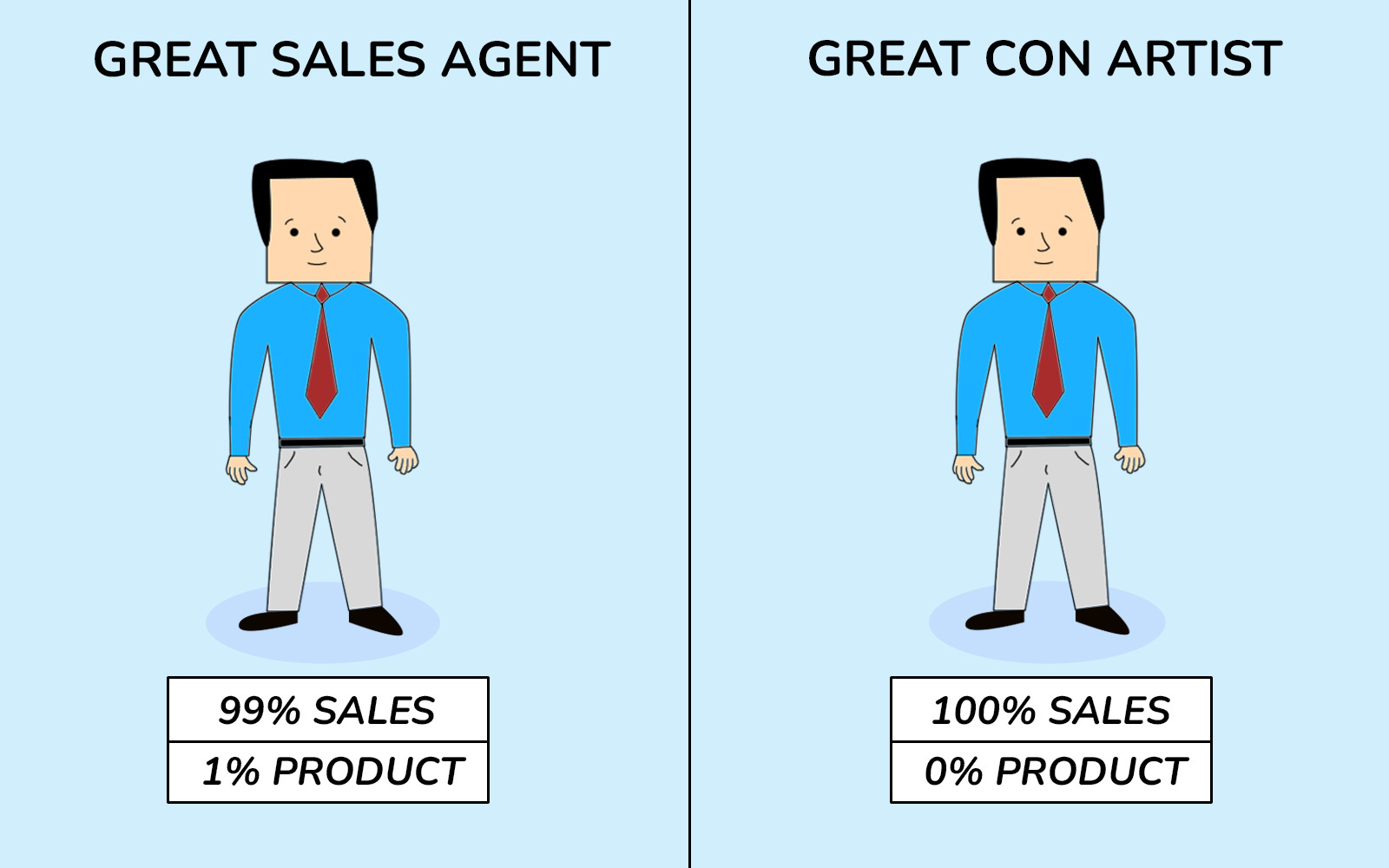

Distinguishing between a great sales agent and a great con artist isn’t always discernable at the onset of the engagement. We generally are able to understand the subtle difference only after the point of sale.

The pretext of this Substack is to allow me a space to use my expertise and experience in finance and insurance to help the general public understand the inner workings of how these industries work so that they can make better financial decisions for themselves and their families.

Financial planning and insurance products can provide immense value.

But because financial services and insurance products are designed and sold based on the psychological preferences and fears of the population looking to buy them, many people end up getting taken advantage of instead being helped by them.

As I’ve alluded to previously, it is human behavior that is the primary driver behind the creation and marketing of these products—not the financial benefits they provide.

So the first step in making better financial decisions for ourselves is to have a deep understanding of who we are as people, our value system, and whether our biases get in the way of actually achieving the outcomes we say that we want.

If we can’t identify our biases prior to making financial decisions then we allow ourselves to become prey to the predatory products and sales practices from companies that understand our biases better than we do and utilize that knowledge against us.

It is asymmetric information in a transaction that allows one party to benefit at the expense of the other.

So while this Substack is explicitly about helping others get a deeper understanding of how insurance products and the financial services industry works to help even out the playing field, beyond this primary goal I want to illuminate how the biases we bring to the table prevent us from both understanding the real value that others provide and how these biases get in the way of creating more effective solutions for ourselves on both an individual and a collective level.

This is not a problem that is unique to the financial services industry. It is endemic to almost all parts of human interaction and society.

Understanding how these dynamics are at play in the financial and insurance industry allow us to see how they manifest in the world around us.

And that’s ultimately what I’m hoping to accomplish here.

I want to show you, the consumer of financial products and services, how the industry I’m a part of uses your own biases, lack of knowledge, and fear against you in order to make profitable products for us that will benefit some of you, but will harm a lot more.

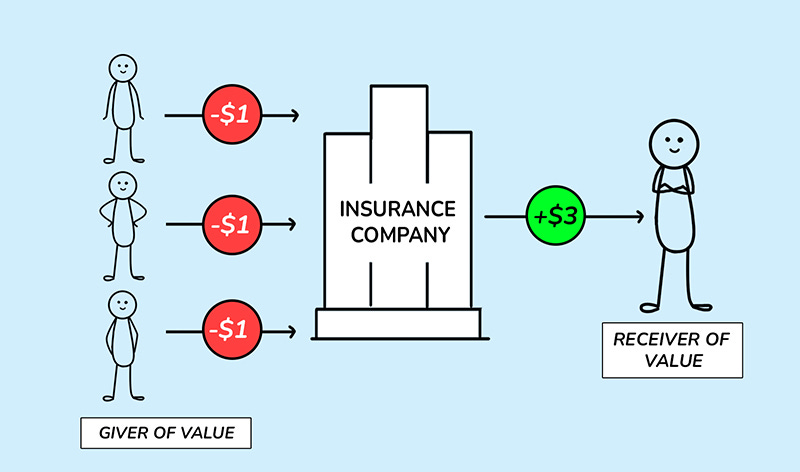

That’s ultimately how most insurance systems work. Some people pay more into the system than others than they receive back, and others extract more value from the system than they pay in. You can’t have one without the other.

But you can understand the game that is being played here and use that to your advantage so that you’re on the winning side.

Unequal Distribution Between Payment and Value

And I’m hoping you’ll take that understanding and apply that to the world around you in a way that gets you to question why so much of the world we live in operates in this “Zero-Sum” game where certain people have to lose so that others can benefit.

And why the people who lose come from a completely different socioeconomic background than the people who win.

It's a regressive system that hinders progress more than pushes it forward.

But if enough of you understand the dynamics of the game and how it’s played and use this to your advantage instead of playing into the hands of the makers of the game, then the companies that create the game are forced to adapt.

That’s the benefit of a free market in which both parties are equipped with the same information.

These companies can no longer rely on an uninformed populace and are forced to create new products and systems that rely less on exploitative mechanics and more on competitive dynamics that are more efficient, cost-effective, and equitable for the consumers that purchase them.

That’s how industries and societies evolve—by designing and implementing more efficient products and systems that create more value for society as a whole instead of merely extracting value from one party and giving it to another.

Equal Distribution Between Payment and Value