#26: Borrowing at Treasury Rates Instead of Mortgage Rates

Most people don’t realize you can borrow against your stock portfolio in a similar way to how you can borrow against your real estate investments—but with better rates and payback provisions

Real estate investors often tout the benefits of investing in real estate.

However, the biggest value that real estate offers over traditional public equity (i.e. stock market) investing is the use of leverage.

So if I’m getting rental income of about 5% of the value of my investment and appreciation rate of 3% then I have a total return of 8% (prior to taxes). And if I’m borrowing at 6% then I have a 2% spread over what the underlying investment is making versus what it costs me to borrow the money.

So I’m making that 2% spread as equity.

2% doesn’t sound like a lot, but it is when we keep in mind that I’m making that 2% spread on the entire value of the property but I only put down 20%.

So let’s do some simple math here.

Let’s say I purchased a $2 million property and put down 20% or $400k and borrowed the remaining $1.6 million at 6%.

Let’s assume I’m making 8% on the $2 million property. That means the return on the property (8%) is greater than the cost of borrowing (6%).

I’m making $160,000 on returns against a borrowing cost of $96,000 (6%*$1,600,000) for a profit of $64,000.

But I only put down $400,000.

So my return on capital is 16% ($64,000/$400,000=16%).

So even though the property is only making 8%, I’m making 16% on my money because I only put down 20% of the cost of the property and borrowed the rest.

And that’s the value of using leverage and earning a spread between the cost of the leverage and what the underlying investment is earning.

And this is the key thing I want people to take away from this article.

Everyone makes real estate out to be super sexy and attractive.

But the real attraction here is the ability to lever up your investment to 80% and make money off the spread between what you’re borrowing at and what you’re earning.

That’s what allows me to earn 16% on my money when the property itself is only netting 8%.

The part that shocks me here when talking to real estate investors is that everyone is so comfortable levering up their real estate investments to 80% or more in spite of the huge mortgage liabilities that come with it—especially when the rental property isn’t cash flow positive.

They do this because they want to turn that 2% spread on other people’s money into a 16% return on their own money.

And yet few people consider the value of using leverage with their investment portfolio.

Even though borrowing against your investment portfolio can be done at significantly lower rates than current mortgage rates and when done properly, you never have to pay back the loan until you sell the investments or die.

In other words, you borrow the money against your portfolio and there is no monthly mortgage payment.

You just pay off the loan when you sell the investments—or better yet you keep the investments for life so that your beneficiaries get the investment tax-free through step-up in basis and pay off the loan at death.

If you’re investing for the long-term on anything and planning on passing on your investments to the next generation—be it real estate or stock investments—then step-up in basis is your friend.

The benefit of borrowing against your investments in both cases is that you get to access the current gains in your investment without paying taxes and losing out on future gains (because you sold the investment).

And much like mortgage interest, the interest here is deductible against your gains (both now and in the future).

Below is a quick comparison between borrowing against your real estate investment (eg a mortgage) and borrowing against your portfolio holdings (eg via box spread loans).

Mortgage Loan vs Box Spread Loan Comparison

The first thing that should stand out from the following table is how low the box spread loan rates against your portfolio are versus mortgage rates.

And that’s because you can borrow against your portfolio at essentially Treasury note rates by using what’s known as box-spread loans. Treasury note rates are significantly lower than mortgage rates due to the higher risk associated with mortgage defaults as opposed to Treasury defaults (i.e. the average person has a higher chance of defaulting on their mortgage over the term of the loan than the U.S. does on their debt over the next 1-5 years).

So if we’re purchasing a house and looking to take out a mortgage at today’s rates, it would be much more efficient to borrow against our portfolio at 4%-4.5% to pay for the house than to borrow at current mortgage rates.

The risk of course is that it’s a variable rate and if interest rates increase in the future then your borrowing rate will increase—as opposed to a mortgage rate where you are locking in the rate for 30 years.

Also you can’t safely borrow as much against your portfolio as you can against the value of your house.

But if the amount you are borrowing is low enough relative to the underlying portfolio, should interest rates dramatically rise you essentially can choose a combination of the following:

1) Invest for the long-term with the assumption that high interest rates will revert to long-term means

2) Use the cash that you would have saved from not having to pay a mortgage to pay down a good portion of the loan

3) Sell off part of your portfolio to pay off the loan

Most people forget the value of options 2 and 3.

Namely, that if the value of your loan balance against your portfolio is low enough then you never have to pay it back until death. So you don’t have to pay the loan back the way you are required to do with a monthly mortgage.

With a mortgage you have a monthly liability to worry about.

When you borrow against your portfolio you don’t have a monthly liability—you just have a long-term loan-to-value (LTV) potential liability.

But as long as you keep your LTV low and/or have ongoing income/cash you can utilize to reduce the LTV then this is an extremely manageable problem.

For example, the money that would have been used to pay the mortgage is essentially freed up to either invest in (thereby lowering the LTV against your portfolio) or to pay down the loan should interest rates rise.

Also, most people when purchasing a home sell part of their portfolio to afford the down payment. Doing this removes that money from the market and earning returns going forward. So selling part of your portfolio down the line to pay off the loan should interest rates rise is not entirely different than selling it at the beginning to afford the down payment.

In both cases you are selling off part of your portfolio to pay for the house.

The only difference is if you put a down payment on a house then you are selling part of the portfolio upfront, versus if interest rates rise later and you want to pay down the loan you are selling part of your portfolio later in order to pay it down.

Hopefully there is an arbitrage for you where you earned more from staying in the market longer than the intermediate cost of the interest on the loan.

Interest rate risk is a serious consideration when borrowing against your portfolio for 30 years—one you don’t have to worry about if you lock in a 30 year mortgage.

But exclusively using a 30 year mortgage removes the opportunity to use a lower variable rate as well as the value of not having a monthly liability hanging over your head every month.

Ideally you are using some combination of a variable rate and a fixed rate when borrowing. When long-term interest rates are high perhaps you are using the lower short-term variable rates. Then when long-term rates are low, perhaps you are locking in the longer term fixed rate at that time.

The point being is that value of the lower cost of borrowing and not having an ongoing mortgage liability every month has to be weighed with the interest rate risk considerations here.

So with this information in hand, it’s important to ask the question:

“What’s the value of levering my real estate investment vs my stock portfolio?”

While I can’t determine what the future will be, I can look at historical stock market returns, home price appreciation rates, rental rates, and mortgage rates and see what the value would have been.

Let’s assume we’re looking at 30 year IRRs starting in 1971 (when mortgage rate data is accessible).

So for 1971 we’d be looking at the period from 1971 through 2000 and for 1996 we’d be looking at the period from 1996 through 2025.

To make this apples to apples we’re going to assume a leverage ratio of 80% to start off with for both the stock market and the real estate investment. We’re also going to assume all dividends (eg rental income) are reinvested in the underlying investment.

To keep this apples to apples we’re not going to assume that the loan is paid back in either case. We’re just going to assume that loan continues to grow for both portfolio borrowing as well as on the real estate side. In other words, there is no traditional mortgage. Just a growing loan balance.

We’re also going to assume optimal investor behavior when it comes to real estate and assume that people refinance their mortgages when interest rates drop.

So given all that, what’s the historical average unlevered and levered 30 year return for both the stock market and real estate if we look back 30 years starting from the year 2000 and through 2025?

The answer is below:

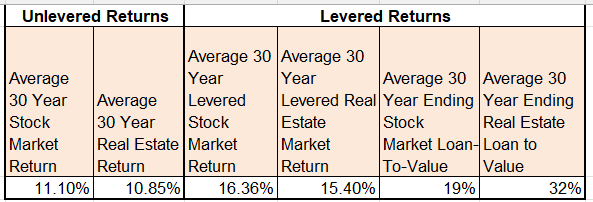

30 Year Look Back IRRs 2000-2025:

Stock Market vs Real Estate on an Unlevered and Levered Basis

Source (Stock Market Returns, Treasury Rates): https://pages.stern.nyu.edu/~adamodar/

Source(Home Price Returns): https://fred.stlouisfed.org/series/CSUSHPINSA

Source (Mortgage Rates): https://www.freddiemac.com/pmms

Source (Rental Cap Rates): https://www.crews.bank/blog/charts/history-of-rental-rates

What’s notable here is that the unlevered returns is that the average stock market unlevered returns are only 25 basis points higher than the average 30 year real estate investing IRR. But leverage makes the stock market returns 100 basis points better.

And the reason for this is that the cost of borrowing against the stock market is lower than that of real estate.

And so the value difference is more pronounced when we look at the levered returns because of this lower cost of borrowing.

We can see this by looking at the average LTV at the end of 30 years. It’s only 19% for the levered stock market returns but 32% for real estate.

For those wonky individuals like myself who want to see/play with the data and the analysis, here’s a link to the full file:

Appreciating the Value of Leverage

The takeaway from this hopefully isn’t that you should lever up your stock portfolio to 80%.

In fact levering up your portfolio to 80% will run the risk of a margin call unless you are actively contributing funds to invest going forward that will lower the LTV.

But it should be to get you to appreciate the value of leverage when so often debt has a negative connotation.

This is especially ironic given that real estate investing has such a positive connotation.

But the real value of investing in real estate comes from the leverage.

And if I can get that same leverage at lower rates and better payback provisions without any of the active time investment that real estate investing requires of property owners, then why am I not looking at utilizing leverage with my stock investments?

If you’re interested in learning how to use leverage with your portfolio to either manage your withdrawals without paying taxes, or to proactively buy into the market, then book a call with us using the link in my bio below.

About the Author

Rajiv Rebello is the Principal and Chief Actuary of Colva Insurance Services and Guaranteed Annuity Experts. He helps HNW clients implement better after-tax, risk-adjusted wealth and estate solutions through the use of strategic planning and life insurance and annuity vehicles. He can be reached at rajiv.rebello@colvaservices.com.

You can also book a call directly with him here:

Yes, it's so hard to get people to acknowledge their own cognitive and emotional biases to investing. So often we make decisions on how we feel and then call it logic. And I think people are so focused on paying down the loan to reduce LTV when in reality if your cost of leverage is lower then it allows the LTV to reduce to a larger extent simply through appreciation